NOW STILL A GOOD TIME TO BUY WATERFRONT?

The memory that makes the numbers worth running.

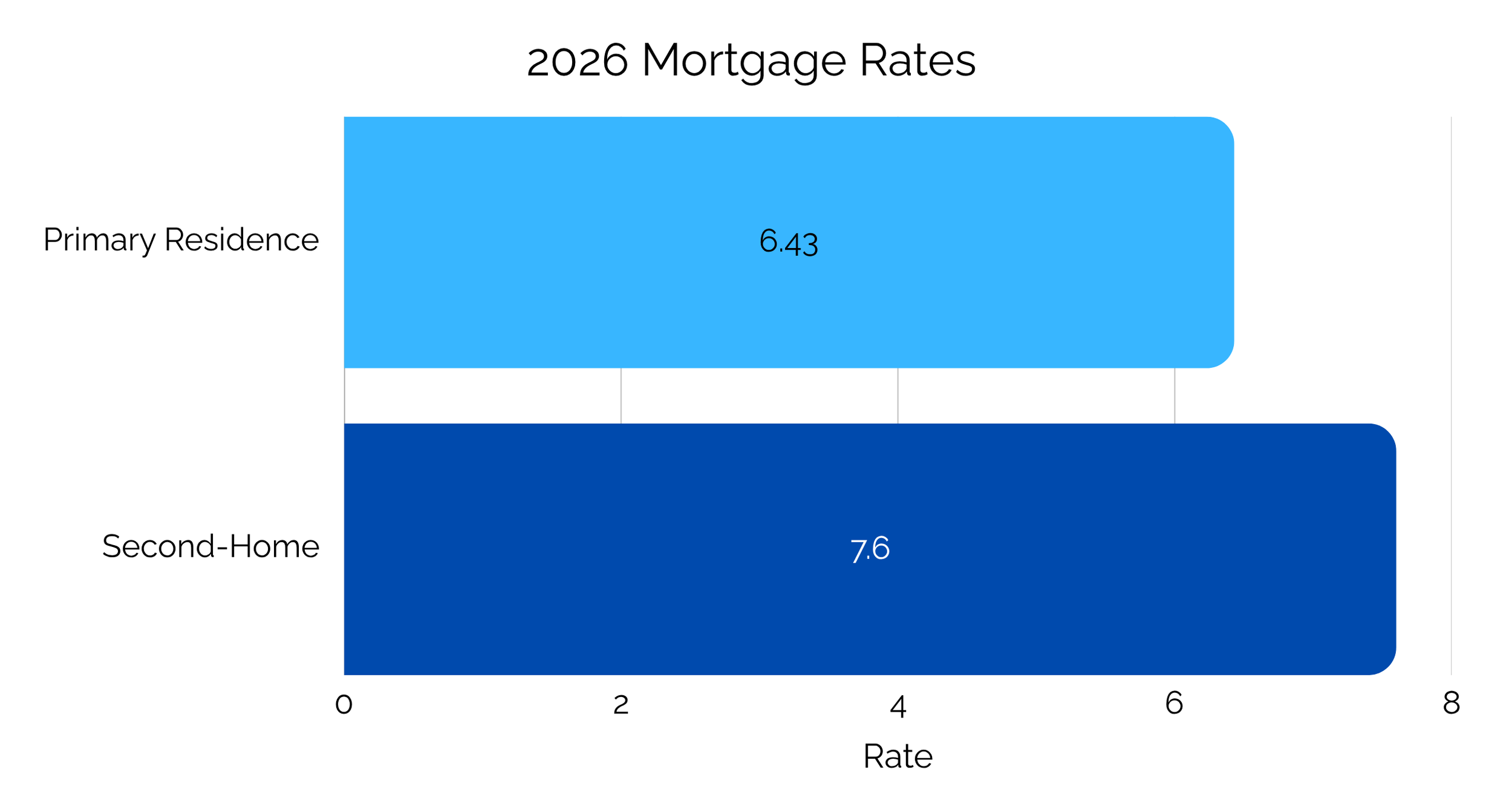

If you’ve found yourself lingering over a listing on the Rappahannock or the Bay, hesitating as you watch rates shift and seasons turn, you’re in good company. Second-home mortgage rates are hovering near 7.6% this summer, a figure that can give even the most committed dreamers pause. Yet, a rate that’s higher than yesterday’s is not the same as a dream that’s out of reach. The real question is what these numbers mean for those drawn to the water’s edge right now—and why, beneath the surface, the opportunity may be more inviting than it first appears.

The rate picture, honestly.

In early July 2026, the 30-year fixed rate for a primary home is 6.43%, its lowest level in weeks. For those seeking a second home, the rate edges higher—around 7.6% for buyers with strong credit. That difference is real, and it deserves honest consideration. Lenders see second homes through a cautious lens, so a larger down payment—think 20% or more—remains your best tool for easing the numbers. Yet, quietly, rates have been drifting downward, not climbing. If you’ve been waiting for the perfect moment, you may already be standing in it.

Why waiting on rates can cost more than it saves

It’s natural to wait for a lower rate, at least on paper. But while you wait, the shoreline does not pause for you. Prices have quietly risen—up 3% across Virginia this spring—and the Northern Neck market is steady, not slowing. Inventory has nudged upward, but true waterfront remains rare: Northumberland County offers just about 100 such listings, a slender offering in a landscape where new shoreline is never made. You can always refinance a rate. You cannot reclaim a view that’s slipped away, or a stretch of water that now belongs to someone else. Sometimes, a slightly higher rate on the home you truly want is the wiser bargain than waiting for a number that may never arrive.

What’s actually different about the waterfront market right now

Two quiet shifts are shaping the waterfront market this year. First, a steady current of out-of-state buyers—many from the D.C. area—are seeking not just a house, but a new rhythm of life, one less tethered to the daily commute. This is not a passing trend but a broader shift in who is drawn to these shores. Second, today’s buyers are more thoughtful and more deliberate than they were during the fevered days of 2021 and 2022. Homes linger a little longer, selling close to list price rather than far above it. The market has found its breath again. Well-priced, well-presented waterfront homes still find new owners, but the frenzy has faded. For buyers, this means genuine competition for the best places, but also the rare luxury of time—to consider, to inspect, to imagine your own story unfolding by the water.

Making the financing work for you

There are a few thoughtful ways to soften the impact of a second-home rate:

• Put more down. Every percentage point above 20% typically chips away at your rate and your mortgage insurance exposure.

• Shop more than one lender. Second-home pricing varies more between lenders than primary-residence pricing does — it’s worth getting three quotes, not one.

• Ask about a temporary buydown. Some sellers and builders are offering rate buydowns for the first year or two of the loan, which can matter a lot if you expect to refinance once rates ease further.

• Budget flood and hazard insurance early. On the water, insurance can move the monthly number more than the rate does — get a quote before you’re under contract, not after.

The question that truly matters

Rates will ebb and flow for as long as you own your home. What remains is the shoreline, the dock, the view that first called you here—the reasons you began your search. If the place and the life it offers feel right, a 2026 rate is simply a point of conversation, not a reason to let another season slip by. If you’re considering a particular property or simply want a clear sense of what a purchase looks like in today’s market, we’re here to help. We guide Northern Neck and Middle Peninsula buyers through these decisions every week. You can also sign up for property alerts to discover new waterfront properties as they appear.